The semiconductor industry is at a pivotal moment. Generative AI is not merely increasing demand for memory; it is triggering a historic, structural "supercycle" that is resetting market fundamentals, rewriting procurement rules, and redefining competitive landscapes. Briocean's latest strategic report, "AI-Driven Memory Supercycle: 2025-2027 Strategic Outlook," provides a comprehensive analysis of this transformation.

📊 The Data Defining the Cycle

$1 Trillion: Projected semiconductor market revenue in 2026 (Omdia).

85-90%: Forecast 2026 growth for the Memory IC segment, driving the industry (Omdia).

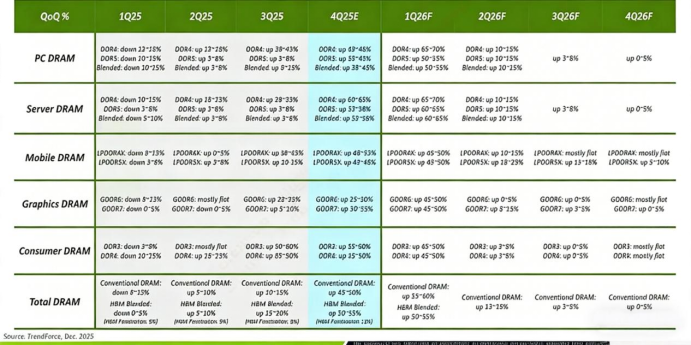

55-60%: Expected Q1 2026 QoQ price hike for DRAM & NAND contracts (TrendForce).

H1 2027: Earliest projected return to market balance.

Is Scarcity Redefining the Entire Market?

The scale of the shift is unprecedented. Omdia projects the total semiconductor market will surpass $1 trillion in revenue in 2026, with the Memory IC segment itself forecast to grow by 85-90%. This explosive growth, visualized below, is overwhelmingly driven by memory, underscoring its role as the engine of the industry.

Figure 1: Greatest Market Contributors to Semiconductor Revenue Growth in 2026

Source: Omdia

This growth stems from a severe structural imbalance. AI's insatiable demand for High Bandwidth Memory (HBM) and high-density server DRAM collides with a supply side that is strategically constrained, as manufacturers reallocate wafer capacity toward these high-margin products. The result is a pricing environment of historic volatility.

As the forecast shows, DRAM and NAND Flash contract prices are projected to rise 55-60% QoQ in Q1 2026. The distortion is even more acute in the spot market, where legacy DDR4 prices have skyrocketed from approximately $7 in mid-2025 to over $78 by January 2026.

⚡️The Critical Question: With pricing power decisively shifted to suppliers and a supply-demand balance not expected before H1 2027, how should procurement strategies evolve from cost negotiation to securing long-term capacity in this new allocation-based paradigm?

Can Your Supply Chain Withstand the DRAM & HBM Squeeze?

Within the memory market, the dynamics for DRAM and HBM are particularly acute, presenting a bifurcated set of challenges.

The DDR4 Paradox: A Costly Legacy Reliance. As the industry races toward DDR5 and HBM, the accelerated phase-out of legacy DDR4 has created a severe supply vacuum. This has led to the extraordinary inversion where DDR4 spot prices now command a significant premium over DDR5. This "scarcity paradox" transforms a mature technology into a high-risk, high-cost component.

The HBM Fortress: Sold-Out and Inaccessible. High-Bandwidth Memory (HBM) is the non-negotiable fuel for AI accelerators. The defining market feature is that effectively all 2026 HBM capacity from major suppliers is pre-allocated to key AI vendors via long-term agreements (LTAs). The competitive race is now for HBM4, but new greenfield fabrication capacity will not arrive meaningfully until 2027-2028.

⚡️The Critical Questions: How exposed is your supply chain to the escalating cost and risk of legacy DDR4? Furthermore, in a market where HBM is effectively sold out, what is your strategy for AI advancement if you cannot secure this critical component?

Is NAND Still a Commodity, or a Strategic Cornerstone?

The NAND Flash market is undergoing a parallel, structural reinvention. It is breaking decisively from its historical, consumer-driven cycles to become a strategically essential asset for AI data pipelines, as evidenced by its evolving revenue trajectory.

Figure 3-1: NAND Flash Revenues and 3D NAND Evolution Trends

Source: Counterpoint Research

The demand driver is clear: petabyte-scale AI data lakes require high-capacity QLC-based Enterprise SSDs. In response, dominant suppliers like Samsung and SK Hynix are exhibiting remarkable capital discipline. They are strategically managing and even reducing output to prioritize profitability over market share, a calculated move that further tightens supply and solidifies their pricing power in the high-margin enterprise segment.

⚡️The Critical Question: As NAND transforms from a cyclical commodity into a supply-controlled strategic asset, what steps are necessary to adapt storage architecture and vendor strategy to this new reality of inelastic demand and manufacturer-led supply discipline?

Navigate the New Landscape with Data-Driven Strategy

The questions posed above highlight the urgent strategic gaps and decisions facing the industry. The transition from a buyer's to a seller's market demands a fundamental rethink of procurement, supplier relationships, and technology planning.

Our full Briocean "AI-Driven Memory Supercycle: 2025-2027 Strategic Outlook" report provides the deep analysis required to answer these questions. It includes detailed quarterly forecasts, comprehensive competitive analysis of major manufacturers, an assessment of geopolitical and supply chain risks, and frameworks for building resilience.

For a confidential discussion on these market dynamics, contact our team of experts.

Follow us on LinkedIn to receive the latest QA and market updates!