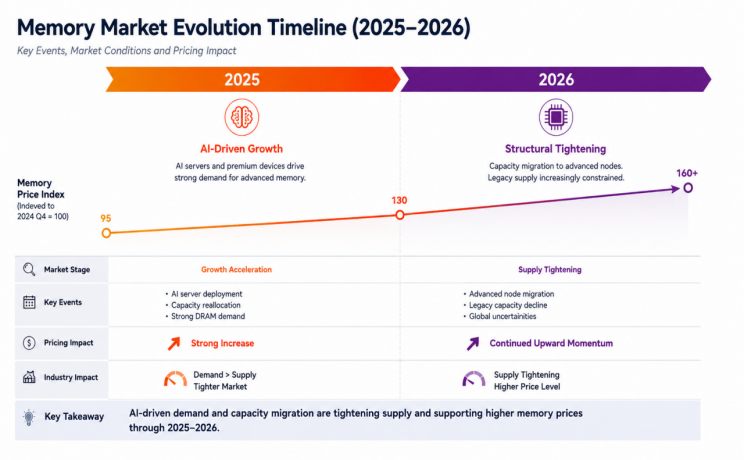

For decades, memory pricing tracked PC and smartphone demand cycles. That era has ended. Today, capacity allocation, AI infrastructure investment, technology migration, and geopolitics are the dominant forces — making pricing less responsive to traditional demand and far more complex for procurement.

Figure: Memory market evolution — from cyclical demand swings to structural supply-driven dynamics

I. AI Demand as a Core Anchor

AI remains the primary driver of memory demand

Micron reports sustained strength in AI-driven memory and HBM growth (Source: Q3 FY2026 Earnings)

AI infrastructure directly supports advanced DRAM pricing

Suppliers increasingly allocate capacity based on AI demand

II. Capacity Shifts Reshape Supply

Samsung and SK Hynix expanding HBM production capacity

Next-generation memory prioritised over legacy nodes

Legacy DRAM and NAND output expected to remain constrained long-term

Supply tightening across automotive, industrial, and embedded segments

III. Disciplined Supply Management, Not Demand Recovery

Major suppliers maintaining cautious production discipline

Pricing stability supported by structural supply management (Source: Counterpoint)

No broad consumer demand recovery required to sustain current pricing

IV. Recent Pricing Trajectories (2025–2026)

Segment

Key Products

Trend

DRAM

DDR3 / DDR4

Sustained upward momentum as legacy supply tightens

DRAM

LPDDR4

Sharp rise driven by automotive (ADAS, intelligent cockpit) and industrial demand

NAND Flash

eMMC

Notable appreciation from early 2026 on tighter NAND supply and shift to premium storage

Inside the Full Report:

✔️ Model‑by‑model pricing trends for DDR3, DDR4, LPDDR4, and eMMC

✔️ Supplier capacity allocation and production discipline analysis

✔️ AI's impact on advanced DRAM pricing and legacy supply

✔️ Strategic procurement recommendations for the new market reality

Click the Download button below for the complete report.

✅ For additional sourcing support or to learn more, feel free to reach out at: