April has triggered a synchronized semiconductor price and supply shock. AI demand is pulling capacity forward, geopolitical disruptions are compressing supply, and multiple vendors have executed multi‑round hikes in weeks — this is not a cycle but a structural shift. April 2026 saw second‑round price hikes of 5%–85%, lead times exceeding 40 weeks, and capacity tightening across analog, MCU, and memory.

For full data and analysis, please click Download.

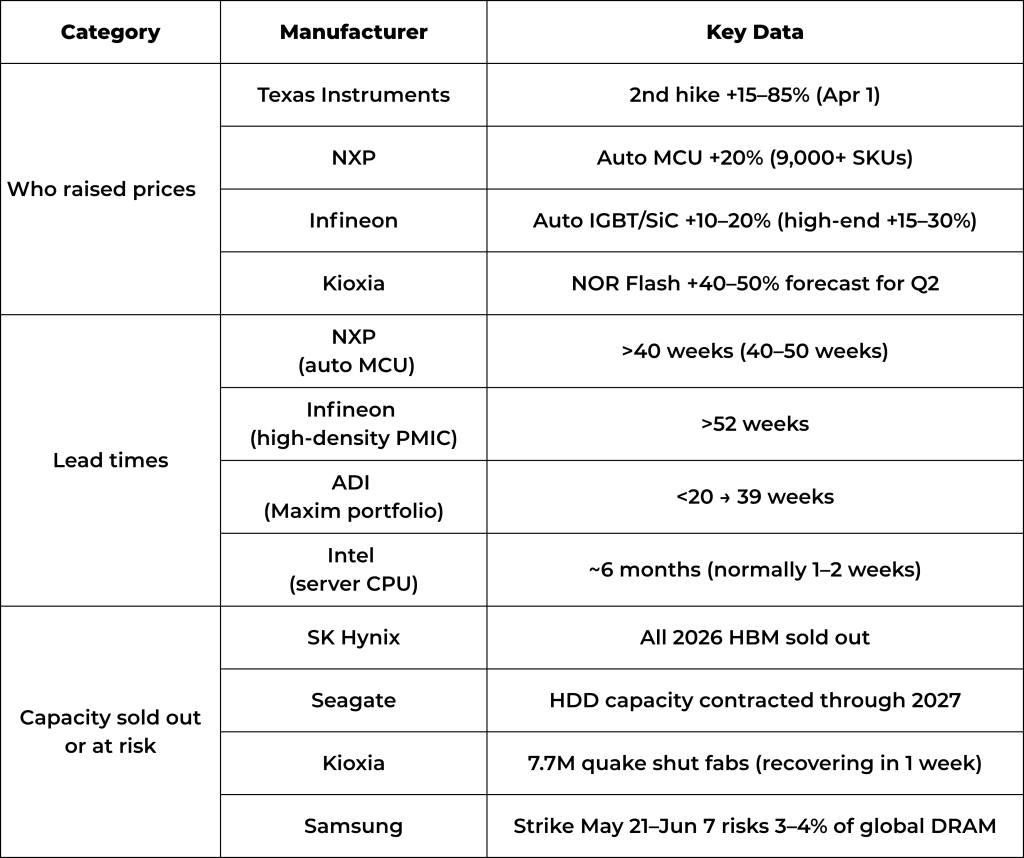

🔴 Critical: What You Need to Know Now

⚡ By Category – One‑Line Summary

Analog & Power: TI (+15–85%), Infineon (+10–20%), ADI (+5–10%, Maxim lead times 39w), Renesas (price hike effective July 1)

MCUs & Auto: NXP (>40w), ST (auto 36–40w, general 12–18w)

Memory: SK Hynix (72% margin, HBM sold out), Samsung (DRAM +30% Q2, strike risk May 21–Jun 7), Kioxia (NOR +40–50%, quake), Micron ($1.8B Taichung fab adds >10% global capacity by 2027)

Computing: Intel (server CPU +10–20%, further hikes expected H2, lead time 6mo), NVIDIA (AI talks with Samsung/SK Hynix)

Foundry: UMC (8‑inch +10–15% H2), TSMC (exit 8‑inch by 2027)

⚠️ Three Structural Risks

HBM eats wafer capacity – 90% of incremental capacity to HBM/server DRAM → conventional DRAM tight. Goldman Sachs: 4.9% DRAM gap in 2026 (worst in 15 years).

8‑inch phase‑out – TSMC exits by 2027; UMC utilization >100% → no quick fix.

💡 Bottom Line

The market is no longer “tightening” — it is structurally constrained. AI has rewritten allocation priorities. Geopolitical and operational disruptions are compounding supply pressure. For buyers: long-term agreements and advance stocking are no longer optional.

Briocean helps buyers navigate this environment with qualified alternative sourcing, vetted global supplier access, quality‑assured procurement, and supply continuity risk monitoring.

📥 Get the full April 2026 report — Download now for complete market insights.